You have been saving for years. Maybe three years. Maybe seven. And every time you check the listings in Oakville, the same thought pops up.

Am I ready to buy, or do I need another year?

If you are searching for down payment first-time home buyer Oakville advice, here is the catch: most people get confused. They hear “20% down” and assume that hitting that number is the only thing standing between them and a home.

Good news. The amount of cash needed up front is just one piece of the puzzle. Your income type, credit, debts, and paperwork all play a role too. With a smart plan, you can put far less down and still walk out with a strong approval.

TL;DR

First-time buyers in Oakville do not always need 20% down. In Canada, the minimum down payment depends on the purchase price, and some homes under $1.5 million may qualify for insured mortgage options. But savings are only one part of the approval. Your income, debts, credit, closing costs, documents, and lender fit all shape what you can actually buy.

Why Oakville Buyers Get Conflicting Advice

You have probably heard all of these in the same week.

- You need 20% down.

- You only need 5%.

- Just open an FHSA.

- Get pre-approved at the bank first.

Each piece is sort of true. None of it is the whole truth. What actually shapes the savings required is the purchase price, the property type, your income, your interest rate, your credit, your debt load, and the source of the funds, including any gifted down payment from family.

Oakville prices are also wildly different depending on what you are buying. WOWA’s May 5, 2026 Oakville Housing Market Report, using April 2026 data, lists average sold prices of:

- $579,135 for condo apartments

- $785,952 for condo townhouses

- $1,076,391 for townhouses

- $1,626,843 for detached homes

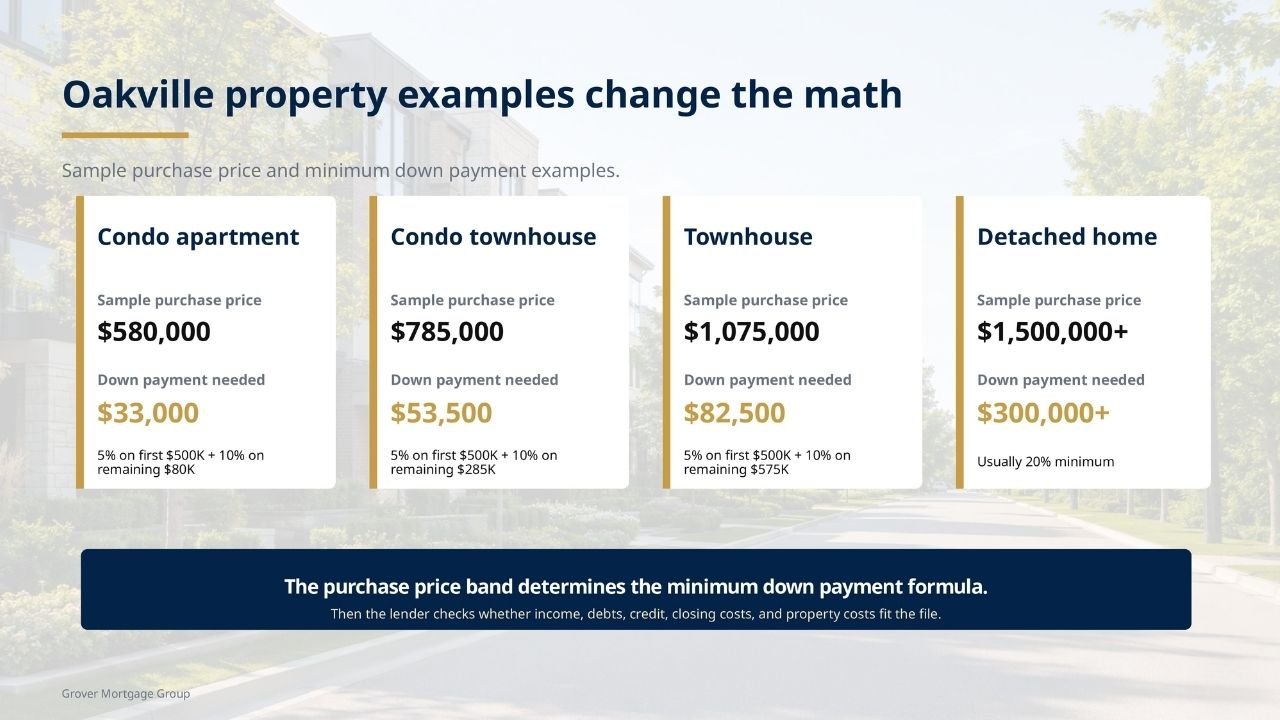

Oakville First-Time Home Buyer Down Payment Examples by Property

| Oakville property example | Sample purchase price | Minimum down payment concept | Total down payment needed |

| Condo apartment | $580,000 | 5% on first $500K plus 10% on remaining $80K | $33,000 |

| Condo townhouse | $785,000 | 5% on first $500K plus 10% on remaining $285K | $53,500 |

| Townhouse | $1,075,000 | 5% on first $500K plus 10% on remaining $575K | $82,500 |

| Higher-priced detached home | $1,500,000+ | Usually 20% minimum | $300,000+ |

Two recent rule changes help Oakville buyers: the federal government raised the insured mortgage purchase price cap to $1.5 million effective December 15, 2024, and expanded 30-year amortization to all first-time buyers and all buyers of new builds.

In plain English, some Oakville condo apartments, condo townhouses, and even townhouses now sit inside the insured mortgage zone, so the savings required might be smaller than you thought. Your mortgage default insurance premium and CMHC rules will apply, and they are part of the math your lender will walk you through.

This is where online calculators fall short: they show a number, but not whether your full file can actually be approved. Closing that gap is what I do every day.

The Down Payment Stack in Your Favour

Your down payment is rarely one number from one account. It is a stack.

- First Home Savings Account (FHSA): The FHSA gives first-time buyers a tax-sheltered way to save toward a qualifying first home. Open it early so the contribution room can build, and pay attention to the withdrawal conditions.

- Home Buyers’ Plan (HBP): The HBP allows a withdrawal from your RRSP toward a qualifying home purchase. It can top up your down payment, but HBP repayment follows a set schedule back into the RRSP.

- Ontario Land Transfer Tax Refund: Qualifying first-time buyers in Ontario can claim a refund of part or all of the provincial land transfer tax. It does not reduce your down payment, but it shrinks the cash you need at closing. Oakville also has no municipal land transfer tax on top, which is one quiet advantage over buying in Toronto.

- First-Time Home Buyers’ Tax Credit: Eligible buyers can claim the federal Home Buyers’ Amount on their tax return. It will not change your upfront numbers, but it can return money to you after the purchase.

- Gifted Down Payment from Family: A gift from immediate family is common in Oakville, and lenders welcome it. CMHC and most lenders require a signed gift letter confirming the money is not a loan, plus proof of funds in your account. Move it in early and the family gift becomes a clean part of your approval story.

The point is simple. Your deposit for the offer, your down payment at closing, and your funds for closing costs can come from different places. The stack only works when every dollar can be traced.

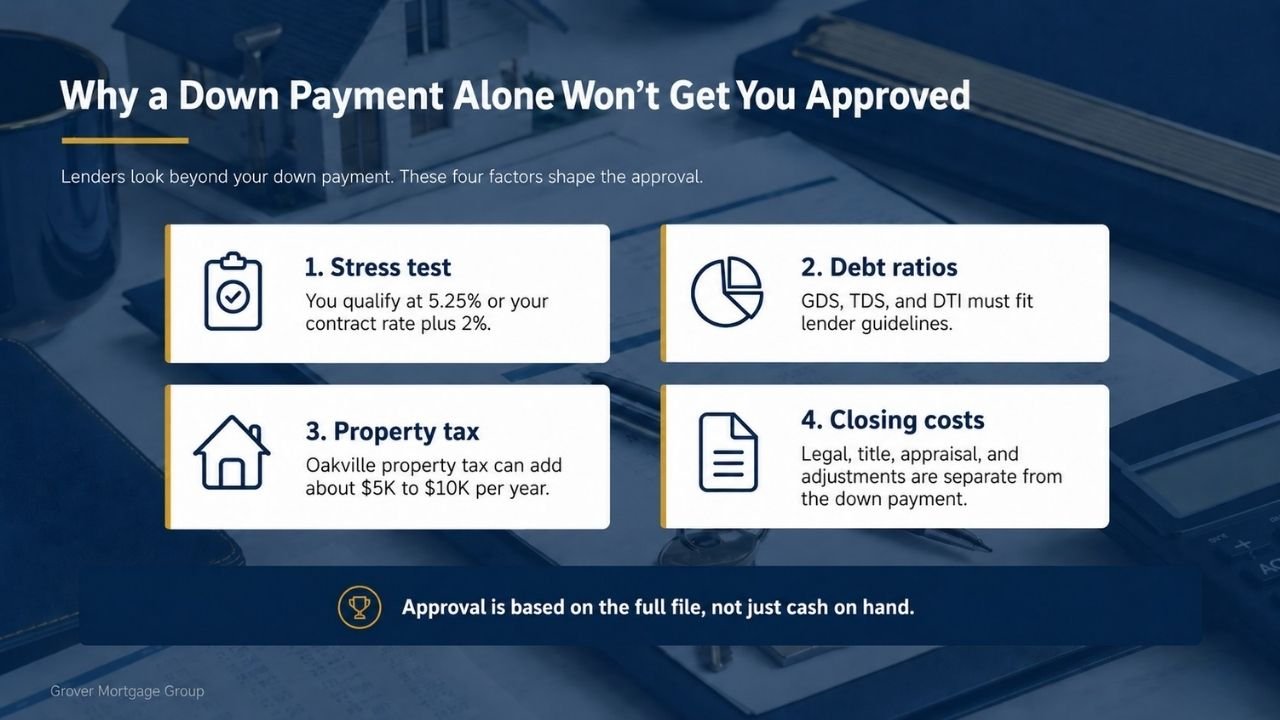

Why a Down Payment Alone Won’t Get You Approved

A lender does not just check your down payment balance. They look at four other things, and any one of them can make or break the file.

- The stress test. Federally regulated lenders qualify you at the higher of 5.25% or your contract interest rate plus 2%.

- Your debt ratios. Your Gross Debt Service (GDS), Total Debt Service (TDS), and debt-to-income (DTI) ratios all need to land inside lender guidelines.

- The full cost of ownership. Property taxes in Oakville often run $5,000 to $10,000 a year, plus condo fees, utilities, and home insurance, and lenders factor them into your ratios.

- Closing costs. Legal fees, title insurance, appraisal, and adjustments for prepaid property taxes, utilities, and condo fees can run into the thousands separately from your down payment.

The most common issue I see with Oakville first-time buyers is not the down payment itself. It is the gap between what they think they can afford and what the lender will approve once income, debts, and closing costs run through the mortgage stress test.

One adjustment often opens the door: a different lender, a longer amortization, a switch between a fixed-rate mortgage and a variable-rate mortgage, or a structure that qualifies as an insured mortgage instead of an uninsured mortgage.

That gap closes faster than most buyers expect once the right lender is matched to the file.

Want to run the numbers yourself first?

My free mobile app lets you pre-qualify without a credit check, see what you can afford, calculate your minimum down payment, and estimate closing costs by city. No sign-up required. Scan the QR code or search for it on the Apple Store or Google Play.

My free mobile app lets you pre-qualify without a credit check, see what you can afford, calculate your minimum down payment, and estimate closing costs by city. No sign-up required. Scan the QR code or search for it on the Apple Store or Google Play.

Want me to review your file before you book another showing? I will review your cash on hand, income, debts, and target purchase range with you. Book a free down payment readiness call or call (289) 208-4469. No pressure, no obligation, just a clear picture of where you stand.

Five Oakville Buyer Scenarios: Which One Are You?

Scenario 1: “We have income, but only $45K to $70K saved”

A condo apartment in the $500K to $580K range may still be in reach as an insured mortgage. The real question is whether your income and debts can carry the mortgage payment, taxes, condo fees, and utilities at the qualifying rate. A clean mortgage pre-approval tells you before you write an offer.

Scenario 2: “Our parents can help, but we do not know how lenders view gifts”

A true gift is fine. You need a signed gift letter, bank statements showing the funds, often a 90-day account history, and proof of funds in your account before closing. Move the money in early and the rest takes care of itself.

Scenario 3: “We are self-employed or commission-based”

Your cash is not the problem. Your taxable income is. Write-offs lower the income a lender can use, so you will need two years of Notices of Assessment, business financials, and a lender that understands non-T4 income. Pre-qualification matters more here than anywhere else.

Scenario 4: “We are new to Canada with income but limited Canadian credit”

Newcomer mortgage programs exist for exactly this. You will need ID, immigration documents, proof of funds, and a plan to build Canadian credit. The earlier you start, the more options you have.

Scenario 5: “The bank declined us, and we do not understand why”

A bank decline is one lender’s opinion, not a verdict. Get the reason in writing, then run the file through a broker who works with many lenders. The same file often gets a yes somewhere else.

Your Oakville Down Payment Readiness Checklist

Work through these in order. By the end, you will know exactly where you stand.

- Set your target price range based on what similar Oakville homes are selling for.

- Calculate your minimum down payment for that price band.

- Add the closing costs: Ontario land transfer tax, legal fees, title insurance, appraisal, and adjustments.

- Tally your savings sources: FHSA, RRSP for the Home Buyers’ Plan, and TFSA.

- Sort out any family help: Gift, loan, or co-buyer arrangement. Draft the gift letter if needed.

- Gather your documents: pay stubs, job letter, NOAs, T4s, bank statements, debt balances, ID, and immigration documents where applicable.

- Review the whole file with a mortgage broker before you sign an offer.

Why a Mortgage Broker Sees Options Your Bank Cannot

A bank sells its own products. One menu. One set of rules. A mortgage broker compares many lenders at once, and that difference matters most when your file is anything other than a textbook salaried T4 buyer with 20% down.

If your file is anything other than standard, you need a lender that reads it the right way. Self-employed, gifted down payment, newcomer, or declined by a bank, each calls for a different door.

At Grover Mortgage Group, I combine big-bank expertise with broker flexibility. I give you access to 70+ lenders across Canada. I offer multilingual mortgage support in English, Hindi, Punjabi, and Urdu. I am clear and responsive. And I have more than $150MM+ in funded lending behind me.

When to Talk to Grover Mortgage Group

You do not need more savings. You need a plan.

Before you put your search on pause, let me review your buyer readiness. I help first-time buyers in Oakville and across the Greater Toronto Area see what they can buy today and what would strengthen the file before they speak to a Realtor.

What you get on a first call:

- A free buyer readiness review of your down payment, income, and debts.

- A first-time buyer mortgage pre-approval walkthrough.

- A second look if a bank has already turned you down.

- A clear plan for FHSA, HBP, TFSA, and gifted down payment sources.

- Service in English, Hindi, Punjabi, and Urdu.

Picture the day you turn the key for the first time. Your address. Your front door. That moment is closer than you think, and it does not start in your savings account. It starts with one honest conversation about your file.

Reach out to Grover Mortgage Group when you are ready to find out.