You have been saving for years.

Oakville keeps rising to the top of your list, and for good reason. Top-ranked schools, waterfront trails along Lake Ontario, a GO train to downtown Toronto in under 40 minutes, and tree-lined neighbourhoods across one of the Greater Toronto Area’s most desirable communities.

You want your first home here. Not somewhere cheaper. Here.

The closing costs, taxes, insurance, and adjustments that pile on top of it? Those are the numbers that actually matter. And nobody lays them out clearly until closing day, when it is too late to plan.

That is what we break down in this post. We walk through the real numbers on a $1.2 million Oakville purchase and a $1.5 million purchase, so you know what to have saved before closing day arrives.

TL;DR

Buying your first home in Oakville takes more cash than most buyers expect.

The biggest extra costs are usually Ontario land transfer tax, legal fees, title insurance, inspection and appraisal costs, moving expenses, and, if you put less than 20% down, the 8% Ontario PST on your mortgage insurance premium, which must be paid in cash at closing.

The fastest way to avoid surprises is to get pre-approved early, understand your real cash-to-close number, and compare your down payment options before you start house hunting.

What are closing costs on a home in Oakville?

Closing costs on a home in Oakville usually include land transfer tax, legal fees, title insurance, inspection costs, appraisal fees, moving costs, and tax or utility adjustments.

How much do you need to buy in Oakville?

For a $1.2 million home in Oakville, buyers typically need about $146,925 to close with 10% down or about $264,247 with 20% down. For a $1.5 million home, buyers typically need about $331,255 to close because homes at that price require a minimum 20% down payment.

How the Down Payment Works on a $1.2 Million Oakville Home

Most first time home buyer guides explain down payments using examples at $400,000 or $500,000. That is not Oakville. The entry point here starts well into seven figures.

As of December 15, 2024, the insured mortgage cap in Canada increased from the $1,000,000 threshold to $1.5 million. If your purchase price is below $1.5 million, you have the option to put less than 20% down and pay mortgage default insurance. Above $1.5 million, that option disappears entirely and a 20% down payment is required. We cover the above-cap scenario later in this post.

Here is how the tiered structure works on a $1,200,000 purchase price:

- 5% on the first $500,000 threshold = $25,000

- 10% on the remaining $700,000 = $70,000

- Minimum down payment = $95,000 (roughly 7.9% of the purchase price)

That $95,000 is the government-mandated floor for an insured mortgage at this price point. Most first time home buyers in Oakville will land in one of two realistic positions: a 10% down payment or a 20% down payment.

Path A: 10% Down Payment ($120,000)

With a 10% down payment, your mortgage is $1,080,000. Because you are putting less than 20% down, mortgage default insurance is required.

At the 10% down payment tier, the premium rate is 3.10% of the mortgage amount. On a $1,080,000 mortgage, that works out to $33,480. This premium gets added directly to your mortgage balance, bringing your total mortgage to $1,113,480.

Ontario also charges 8% provincial sales tax (PST) on the default insurance premium. That PST amount of $2,678.40 cannot be rolled into your mortgage. It must be paid in cash at closing.

One advantage of this path: as a first time home buyer, you are now eligible for a 30-year amortization on an insured mortgage. The longer amortization lowers your monthly payment compared to the standard 25-year mortgage term, though you will pay more interest over the life of the loan.

Path B: 20% Down Payment ($240,000)

With a 20% down payment, your mortgage is $960,000. This is a conventional mortgage. No mortgage insurance. No insurance premium added to your balance.

This path requires significantly more cash upfront. But your mortgage balance is lower from day one, you avoid the $33,480 in default insurance costs, and your monthly payment reflects a smaller loan.

What First Time Home Buyers Pay in Closing Costs in Oakville

The down payment gets all the attention. Closing costs are where first time home buyers get blindsided.

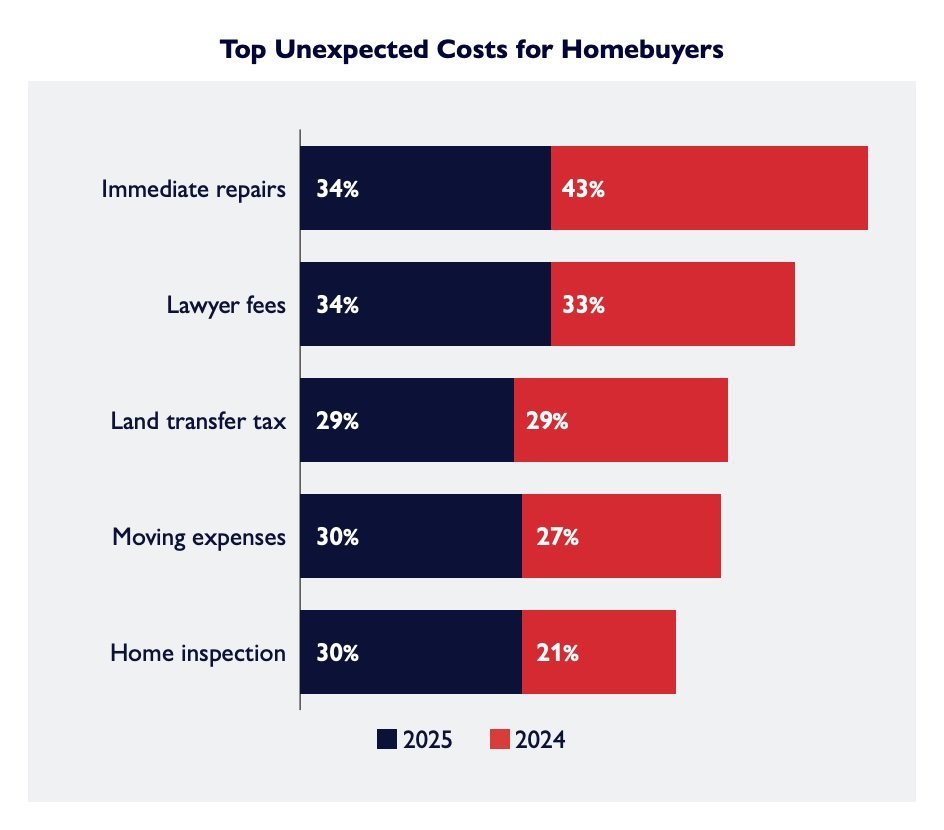

And this is not just our opinion. According to CMHC’s 2025 Mortgage Consumer Survey, 42% of homebuyers in 2025 faced unexpected expenses during the buying process, up from 36% in 2024.

The top surprises? Immediate repairs (34%), lawyer fees (34%), land transfer tax (29%), moving expenses (30%), and home inspection costs (30%).

Every single one of those “surprises” is something we cover below. That is the whole point of this breakdown: if you know what is coming, nothing is unexpected.

According to the Financial Consumer Agency of Canada, you should budget 1.5% to 4% of the purchase price for closing costs on top of your down payment.

CMHC also breaks down the true cost of buying a home beyond the listing price, and the closing cost breakdown is longer than most first time home buyers expect.

The biggest closing cost after your down payment is usually Ontario land transfer tax.

Here is what the full cash-to-close picture looks like on a $1,200,000 Oakville home.

The Full Picture: Cash to Close on a $1.2M Oakville Home

Here is where the two paths diverge:

| Item | 10% Down | 20% Down |

| Down payment | $120,000.00 | $240,000.00 |

| Ontario land transfer tax (net of rebate) | $16,475.00 | $16,475.00 |

| Legal fees | $1,200.00 | $1,200.00 |

| Legal disbursements | $300.00 | $300.00 |

| Title insurance | $900.00 | $900.00 |

| Title insurance PST | $72.00 | $72.00 |

| Home inspection | $500.00 | $500.00 |

| Survey or certificate of location | $1,500.00 | $1,500.00 |

| Appraisal | $300.00 | $300.00 |

| Moving costs | $2,000.00 | $2,000.00 |

| Final adjustments | $1,000.00 | $1,000.00 |

| PST on mortgage insurance | $2,678.40 | $0.00 |

| Lender fee | $0.00 | $0.00 |

| Brokerage fee | $0.00 | $0.00 |

| Estimated cash to close | $146,925.40 | $264,247.00 |

| CMHC insurance (added to mortgage) | $33,480.00 | $0.00 |

A few things to note. The $33,480 insurance on the 10% path is not part of your cash to close. It is added to your mortgage balance, bringing your total mortgage to $1,113,480 instead of $1,080,000. You pay interest on that extra $33,480 for the full life of the loan. What you do pay in cash is the $2,678.40 PST on the premium, which cannot be rolled into the mortgage.

The 20% path requires $117,321.60 more cash upfront. But it means a smaller mortgage from day one, lower mortgage payments, and no insurance premium compounding over 25 or 30 years.

Want to Run Your Own Numbers?

These examples show what buying at $1.2 million can look like, but your numbers may be very different depending on your purchase price, down payment, income, and mortgage option.

These examples show what buying at $1.2 million can look like, but your numbers may be very different depending on your purchase price, down payment, income, and mortgage option.

Use our free mortgage calculator app to estimate your monthly payment, compare down payment scenarios, and get a clearer picture of your potential cash to close before you start house hunting.

No credit check. No pressure. Just a faster way to understand your numbers.

What Changes Above the $1.5 Million Insured Cap

Everything above applies when your purchase price is below $1.5 million. But Oakville has no shortage of homes listed above that threshold, including plenty of Oakville luxury home options.

Above $1.5 million, mortgage default insurance is not available. Period. You cannot put 5% down or 10% down. The only path is a 20% down payment, which means a conventional mortgage with no insurance.

Here is what the numbers look like on a $1,500,000 Oakville home:

| Item | Amount |

| Down payment (20%) | $300,000.00 |

| Ontario land transfer tax | $26,475.00 |

| First time home buyer rebate | -$4,000.00 |

| Legal fees | $1,200.00 |

| Legal disbursements | $700.00 |

| Title insurance | $1,000.00 |

| Title insurance PST | $80.00 |

| Home inspection | $500.00 |

| Survey or certificate of location | $1,500.00 |

| Appraisal | $300.00 |

| Moving costs | $2,500.00 |

| Final adjustments | $1,000.00 |

| Lender fee | $0.00 |

| Brokerage fee | $0.00 |

| Estimated cash to close | $331,255.00 |

Property Insurance: Required Before You Close

Your mortgage lender will require proof of home insurance before they release your funds on closing day. No insurance, no keys.

You will need an active policy with the lender named as loss payee, and your real estate lawyer will ask for the insurance binder before closing. The policy must be effective on or before your closing date.

This is not a closing cost in the traditional sense since you are paying for ongoing coverage, not a one-time fee. But it is cash you need to have arranged before closing day. Start shopping for quotes at least 30 days before your closing date so there are no last-minute surprises.

Pre-Approval, the Stress Test, and What Lenders Actually Look At

Before you start touring homes in Oakville, get a real pre-approval. Not a vague pre-qualification from a bank teller. A full pre-approval where a mortgage broker reviews your file, runs your numbers, and tells you exactly what you qualify for.

At Grover Mortgage Group, I review every file personally and contact you within 24 hours with a clear mortgage path. That is how we work as your mortgage agent.

Here is what many first time home buyers do not expect: your purchase price ceiling is not based on the interest rate you will actually pay. It is based on the stress test.

Lenders qualify you at the higher of your contract interest rate plus 2%, or 5.25%. This qualifying rate determines your maximum purchase price and monthly payment. It is designed to make sure you can still afford your mortgage payments if rates rise. But it also means your mortgage affordability is often lower than you assumed when you were doing the math on your phone.

What do lenders look at beyond the down payment?

- Income verification. T4 slips, recent pay stubs, and a two-year employment history. If you have self-employed income, expect to provide two years of tax returns and business financial statements.

- Credit score. The minimum for an insured mortgage is 600 under current guidelines. A higher score opens the door to better rates and more lender options.

- Debt-to-income ratio. Lenders calculate how much of your gross income goes toward housing costs and total debt obligations. This ratio determines how much mortgage you can carry.

- Proof of funds. You will need 90 days of bank statements showing your down payment and deposit are sourced and seasoned. Gifted deposits from family are acceptable, but they require a signed gift letter.

- Lender conditions. Some requirements only surface between pre-approval and firm approval. These can include updated employment letters, additional bank statements, or property-specific conditions that were not apparent at the pre-approval stage.

What if your situation does not fit the traditional mold? Maybe your income is self-employed, your credit history is short, or you are a newcomer to Canada.

At Grover Mortgage Group, we have access to 70+ lenders, which means more paths to firm approval than any single bank can offer.

In some cases, an alternative lender or a private mortgage may be the right fit to get you started. We also offer multilingual mortgage support, so language is never a barrier to getting the help you need.

With $150MM+ in funded lending and big-bank expertise combined with broker flexibility, we work with a wide range of first time home buyer situations every day. Our service area coverage spans Oakville, Mississauga, Burlington, Hamilton, and the wider GTA. The goal is not to push you toward a product. It is to find the one that fits.

Your First Time Home Buyer Savings Checklist

Before you book your first showing in Oakville, make sure you have accounted for every line item below. Not just the down payment. All of it.

- Down payment. 5% to 20% of your expected purchase price, depending on your chosen path and whether you are above or below the $1.5 million insured mortgage cap.

- Mortgage default insurance. If you are buying with less than 20% down, the CMHC premium is added to your mortgage balance, but the 8% Ontario PST on that premium is due in cash at closing.

- Ontario land transfer tax. Minus the $4,000 first time home buyer land transfer tax rebate.

- Legal fees and disbursements.

- Title insurance.

- Home inspection.

- Survey or certificate of location.

- Appraisal.

- Property insurance. Your lender requires proof of an active home insurance policy before closing. Have this arranged at least 30 days in advance.

- Property tax, utility adjustment, and condo fee adjustments.

- Moving costs.

- Cash buffer. At least $5,000 to $10,000 for post-move essentials, unexpected lender conditions, and the things you do not know you do not know yet.

One more thing worth understanding: when you make an offer on a home, you submit a deposit that is held in trust by the listing brokerage. That deposit becomes part of your down payment.

Having your pre-approval in place and your proof of funds ready strengthens your offer conditions. In a competitive Oakville market, preparation is the difference between winning and watching.

You Have Done the Hard Part

You have been saving. You have done the research. You picked Oakville for all the right reasons.

The numbers in this post might feel heavy. That is okay. Whether you are looking at $1.2 million with a flexible down payment or $1.5 million where 20% is the only option, the point is the same: walk into your home search with open eyes and a clear plan, so nothing catches you off guard between your accepted offer and closing day.

Get a Clear Buying Plan Before You Make an Offer

Before you start touring homes in Oakville, know exactly where you stand.

With a personalized pre-approval from Grover Mortgage Group, we will help you:

- See your realistic purchase price range based on the stress test and current rates

- Compare 10% vs. 20% down payment options side by side

- Understand your full cash to close amount before closing day

- Review monthly payment scenarios based on current mortgage rates

- Move forward with clarity, not guesswork

And if your situation falls outside traditional lending criteria, we can help with that too. For buyers who need a non-traditional path to homeownership, Grover Mortgage Group also offers private mortgage solutions designed to bridge the gap until you qualify with a conventional lender.

Every pre-approval we build is based on your income, your savings, and your goals. Not a generic estimate.

No obligation. No credit check at the inquiry stage. I review every file personally.

Reach out to us at Grover Mortgage Group to get your personalized pre-approval and know exactly what you can afford before you make your first offer.