Your realtor mentions pre-approval. A friend who bought last year brings up pre-approval too. Even the mortgage page you just opened talks about pre-approval.

Everyone seems to assume you already know what it means.

At some point, you probably stopped asking.

I have been a mortgage agent for over twelve years, and I have helped hundreds of first-time buyers in Mississauga through this exact moment. Many arrive at my desk carrying the same quiet question. Most are too polite to say it out loud, so I will say it for them.

What is pre-approval, really? Do you actually need it before you start looking at homes?

Let me show you.

The Short Version

If you only have ninety seconds, here is what you need to know.

- What it is: A pre-approval is a lender’s review of your income, credit, down payment, and debts. It tells you how much a real lender will actually lend you, not what an online calculator guesses.

- When to get it: Before you start booking showings. Skipping this step weakens your offers and slows you down at the worst possible moment.

- What you need: Pay stubs, T4s, Notice of Assessment, ninety days of bank statements, ID, and a list of your debts. Self-employed buyers need a bit more.

- The rate hold bonus: A pre-approval can lock in a rate for sixty to one hundred and thirty days while you shop, which protects you if rates climb.

- The catch: Pre-approval is not final approval. The home itself, the appraisal, and any change to your finances can still affect the outcome.

Getting pre-approved is only one part of buying your first home. For complete guidance on lender options, down payment planning, closing costs, and the full mortgage process, visit our main page for first-time home buyer mortgage broker in Mississauga.

Now let us walk through each piece properly.

So What Is Pre-Approval, Really?

Strip away the jargon and the idea becomes simple.

A pre-approval is a lender’s review of you as a borrower. They look at your income, your credit, your minimum down payment, and your debts. After that review, they tell you what a real lender will actually lend you on a purchase mortgage.

That is very different from what an online calculator estimates. A lender reviews your actual file, your specific debts, and your cash-to-close once closing costs are factored in.

That number changes everything.

It tells you which Mississauga neighbourhoods are realistic and which are wishful thinking. It shows whether you should focus on a one-bedroom condo near Square One or a townhouse in Meadowvale. Most importantly, it prevents you from falling in love with a home you cannot realistically buy.

So yes, you need one. And no, it is not the same as the number you got from a bank calculator online.

That distinction creates most of the confusion, so let us clear it up next.

Pre-Qualification vs Pre-Approval

People use these two words interchangeably. They are not the same thing.

Pre-qualification is a quick estimate. You tell a lender your income and debts, and they give you a rough borrowing range. No documents. No credit check. No real verification.

Pre-approval goes deeper. It usually involves documents, a credit check, and a proper lender review. The Financial Consumer Agency of Canada confirms this distinction, and it matters more than many buyers realize because your credit score and credit history can change the borrowing picture quickly.

There is another layer buyers often miss. Lenders do not all define these terms the same way. Some call a basic estimate a pre-approval, while others reserve that label for a much deeper review.

So when someone says they have been pre-approved, the number itself is only part of the story.

What really matters is how far the lender went. Did they review documents? Did they pull credit? Or did they simply plug numbers into a form?

That is the difference that protects you.

Documents Needed for Mortgage Pre-Approval

A strong file moves faster and gives you a more reliable budget. Here is what I will ask you to gather.

Download our free borrower’s document checklist so you can tick items off as you go.

For employment income: A recent pay stub, T4 slips from the past two years, your most recent Notice of Assessment, and an employment letter where applicable.

For self-employed income: Two years of T1 Generals, Notices of Assessment, business financial statements, and proof of business registration or incorporation.

For your down payment: Ninety days of bank statements, FHSA or RRSP statements if you are using those funds, and a signed gift letter plus source documents if any portion is being gifted by family.

For identification and liabilities: Government-issued photo ID, current housing cost details, and a list of debts including credit cards, lines of credit, car loans, and student loans.

That final category catches more buyers than you would think. A forgotten car payment, an unused line of credit, or an overlooked student loan can shift your debt-to-income ratio more than expected.

Small numbers add up quickly in mortgage qualification.

I would rather catch those details at the kitchen table than at the offer table.

Want me to review your income, down payment, and documents before you start booking showings?

Book a free pre-approval call or call (289) 208-4469. No pressure, no obligation, just a clear picture of where you stand.

Why Pre-Approval Matters Before Showings

Skipping pre-approval and jumping straight into showings creates three major problems. I have watched all three happen many times, and none of them end well.

Problem 1: you fall for the wrong house.

Online affordability calculators do not run the mortgage stress test the same way lenders do. Most calculators also ignore property taxes, condo fees, and heating costs that lenders include in debt service ratios.

As a result, the number you see online and the number you are actually approved for can be very different.

By the time buyers realize that, they have often already imagined their furniture in the living room.

Problem 2: your offers do not get taken seriously.

Sellers and listing agents review every detail carefully. A clean pre-approval letter paired with a short or no financing condition makes you look prepared and reliable.

Without that paperwork, your offer in a competitive Mississauga market often loses to buyers who already have their financing organized.

Problem 3: rates move while you shop.

A pre-approval can include a rate hold that protects you for a set period if rates rise.

Without that protection, your buying power can shrink between your first showing and your accepted offer.

A proper pre-approval also uncovers problems early. Sometimes it is a credit reporting error. Other times it is missing income paperwork, an unexplained down payment source, or a surprise mortgage insurance premium added to the loan.

Finding those issues now is far better than discovering them two days before closing.

How Rate Holds Work

A rate hold reserves a rate for a set period while you shop. The Financial Consumer Agency of Canada states that a pre-approval may lock in an interest rate for sixty to one hundred and thirty days, depending on the lender.

That window acts as your shield.

If rates climb while you are house hunting, your held rate stays in place. If rates fall, many lenders allow you to take the lower rate at closing instead.

Still, a rate hold is not a guarantee. The lender, the property, and the final application continue to matter. Some holds expire if you do not purchase in time. Others come with conditions buyers do not notice until later.

Whenever I issue a rate hold for a client, I explain exactly what is protected, what remains conditional, and when a fresh review could be required. Clear expectations matter.

What Can Still Go Wrong After Pre-Approval

Pre-approval is preparation, not a promise. This is the single most important thing buyers need to understand.

The Financial Consumer Agency of Canada says it plainly. A pre-approval does not guarantee final approval.

An appraisal can come in low. The building may not fit lender policy. Your employment situation may change. New debt can appear. The final file might no longer match the original application.

Buyers who understand this make smarter offers, protect their deposits, and avoid stretching into homes that only worked on paper.

Pre-Approval Letter vs Final Mortgage Approval

These two documents serve completely different purposes. Confusing them can become an expensive mistake for a first-time buyer.

A pre-approval letter focuses on you as the borrower. Based on your income, credit, down payment, and debts, it estimates what you can likely borrow. It is not tied to a specific property and still comes with conditions: satisfactory appraisal, no material change in your finances, and final document verification.

A final mortgage approval focuses on the property itself.

The lender reviews the purchase agreement, appraisal, condo status certificate where applicable, and any updated financial documents. Only after those reviews are completed do the conditions clear and the funds become guaranteed.

That gap between pre-approval and final approval is where financing surprises usually happen.

Your job is to keep that gap small. My job is to guide you through it.

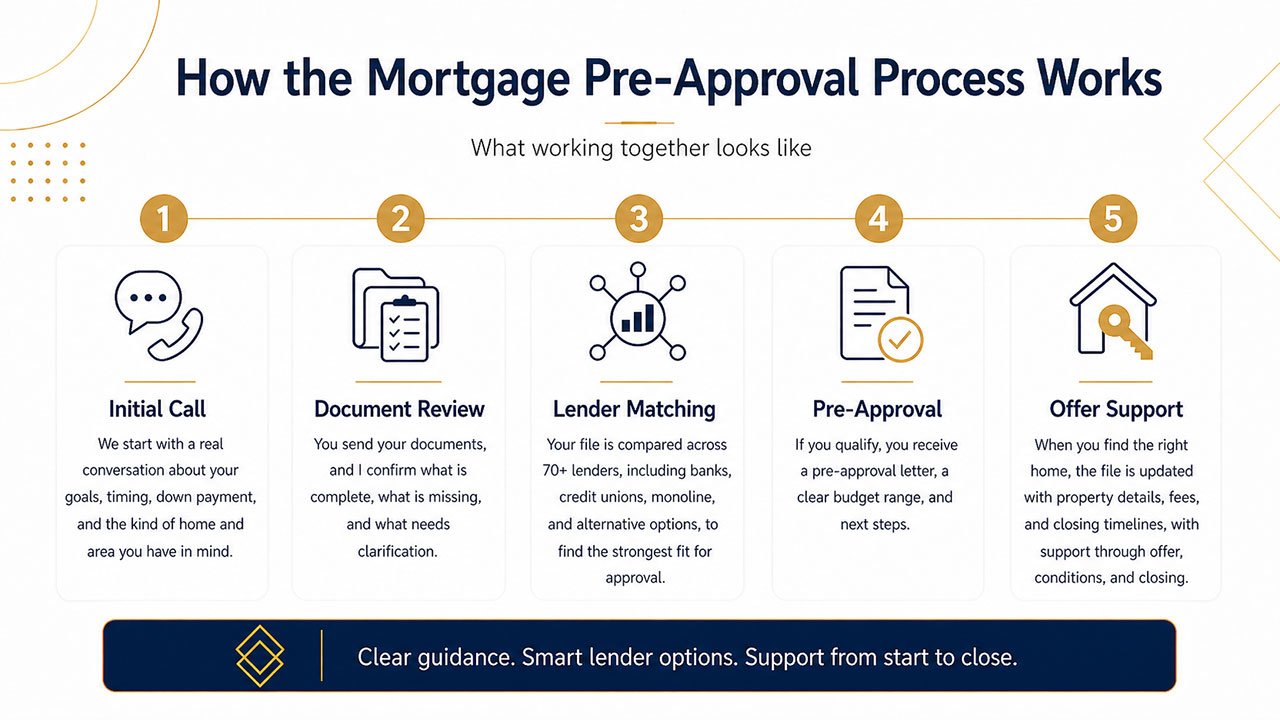

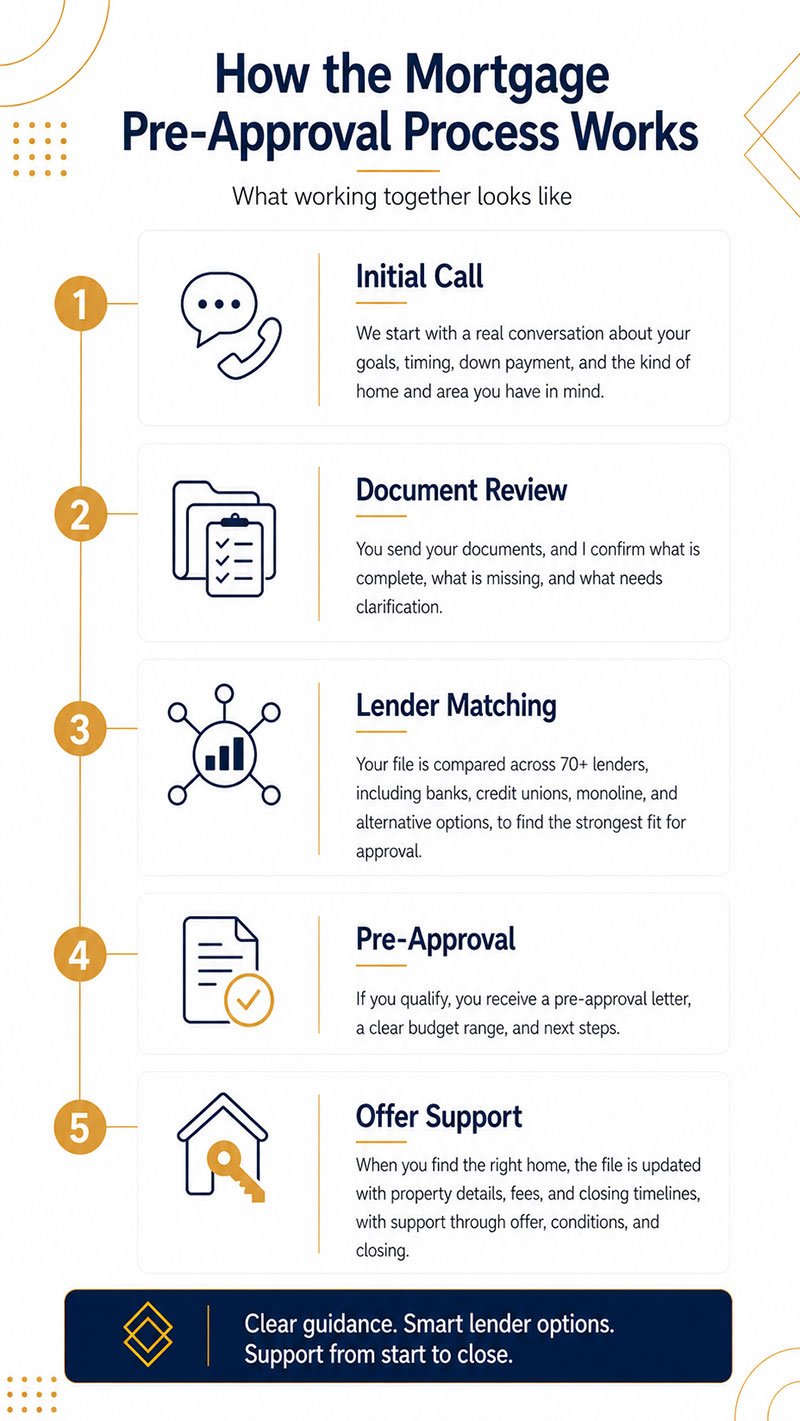

How the Pre-Approval Process Works

Here is what working with me actually looks like.

- A real conversation. We start with a call. I ask about your goals, your timeline, your down payment, and the kind of home you are picturing. Condo, townhouse, freehold. Mississauga, or somewhere else in the GTA. No pressure. No script.

- Document collection. You send over your documents and I let you know exactly what is missing and what is good.

- Lender matching. This is where my access to 70+ lenders becomes your advantage. Real lender comparison means looking past the headline rate, weighing banks against credit unions, monoline lenders, and alternative lenders, and picking the right fit, because a slightly higher rate at a lender who actually approves your file beats a great rate that falls through.

- Pre-approval issued. If you are eligible, you get the letter, the budget range, and a clear plan for what to do next.

- Offer-day support. When you find a home, I update the file with the MLS details, the fees, and the closing date. I am there for the offer, the conditions, and the close.

First-time Buyer Programs Worth Knowing

There are programs that can stretch your dollar further:

- First Home Savings Account: The FHSA lets eligible first-time buyers save toward a qualifying first home with tax advantages. It can help build your down payment, but contribution room and withdrawal rules matter.

- RRSP Home Buyers’ Plan: The Home Buyers’ Plan lets eligible buyers withdraw funds from their RRSP to buy or build a qualifying home. This can support your down payment, but the funds usually need to be repaid over time.

- Ontario Land Transfer Tax Rebate: Eligible first-time buyers in Ontario may receive a refund of all or part of the land transfer tax. This can reduce the amount of cash needed at closing.

- Federal first-time Home Buyers’ Tax Credit: Eligible buyers may be able to claim the federal Home Buyers’ Amount at tax time. This does not reduce your upfront closing costs, but it may provide tax relief after purchase.

Each one helps. None of them fix a weak debt-to-income ratio. They work best when paired with a realistic lender qualification, which is exactly what we will sort out together.

Why Choose Grover Mortgage Group

I am a Mortgage Agent Level 2 with over twelve years of experience and $150MM+ funded lending behind me. I spent years inside RBC, TD, and BMO before I went independent. That means I know how big-bank underwriters think, and I shop beyond a single bank channel for you.

Salaried, hourly, commissioned, self-employed: I have seen the file before. I will give you straight answers about your approval strength, fast replies when you are mid-showing, and offer-day support when the pressure is on.

Multilingual support is available in English, Hindi, Punjabi, and Urdu, which matters if you are a newcomer to Canada navigating your first mortgage and want someone who can walk you through it in your own language.

Mississauga Service Area

I work with first-time buyers all across Mississauga and the wider Greater Toronto Area (GTA). Each pocket of the city brings its own lender questions.

City Centre and Square One condos are the classic entry point. Transit access, lower maintenance, manageable price tags. Port Credit, Clarkson, Cooksville, Erin Mills, and Streetsville come up often for buyers who want a bit of community feel without leaving the city. Meadowvale and Lisgar pull many family-oriented buyers toward townhomes.

Each one triggers different lender questions around condo fees, property type, parking, and resale profile. Local file review matters. I have been doing this in Mississauga for over a decade.

Get a Clear Budget Before You Make an Offer

You started reading this because you were not sure what pre-approval meant or whether you needed one.

Now you know.

You need it. And you do not have to figure it out alone.

Book a free pre-approval consultation with me before you write your first offer. Send me your estimated down payment, your preferred closing timeline, and your income type, and I will take it from there.

The first home is the hardest one. Let us make sure yours is the one you will look back on with a smile.