Here is a myth I hear all the time. “The FHSA is just a savings account with a tax break.”

It is not. Calling it that is like calling a multi-tool a screwdriver. Technically true. Wildly incomplete.

The FHSA, also called the First Home Savings Account or first time home savings account, is one of the rare accounts in Canada that lets you deduct your contributions, grow your money tax-free, and pull it out tax-free, with no repayment. There is nothing else quite like it.

The RRSP gives you the deduction but charges you back later through taxes or repayment rules.

That is the upside. But there is also a catch, and it is the part most articles glide past.

The FHSA helps you build a down payment. It does not get you a mortgage.

I have sat across from buyers who showed me a healthy FHSA balance and assumed the rest would sort itself out. It does not. Your income, your credit, your debts, and your closing costs all still get reviewed by the lender, and none of that lives inside your FHSA.

So let me walk you through how the account actually works, and where I see first-time buyers either gain ground or lose it.

TL;DR

If you only have ninety seconds:

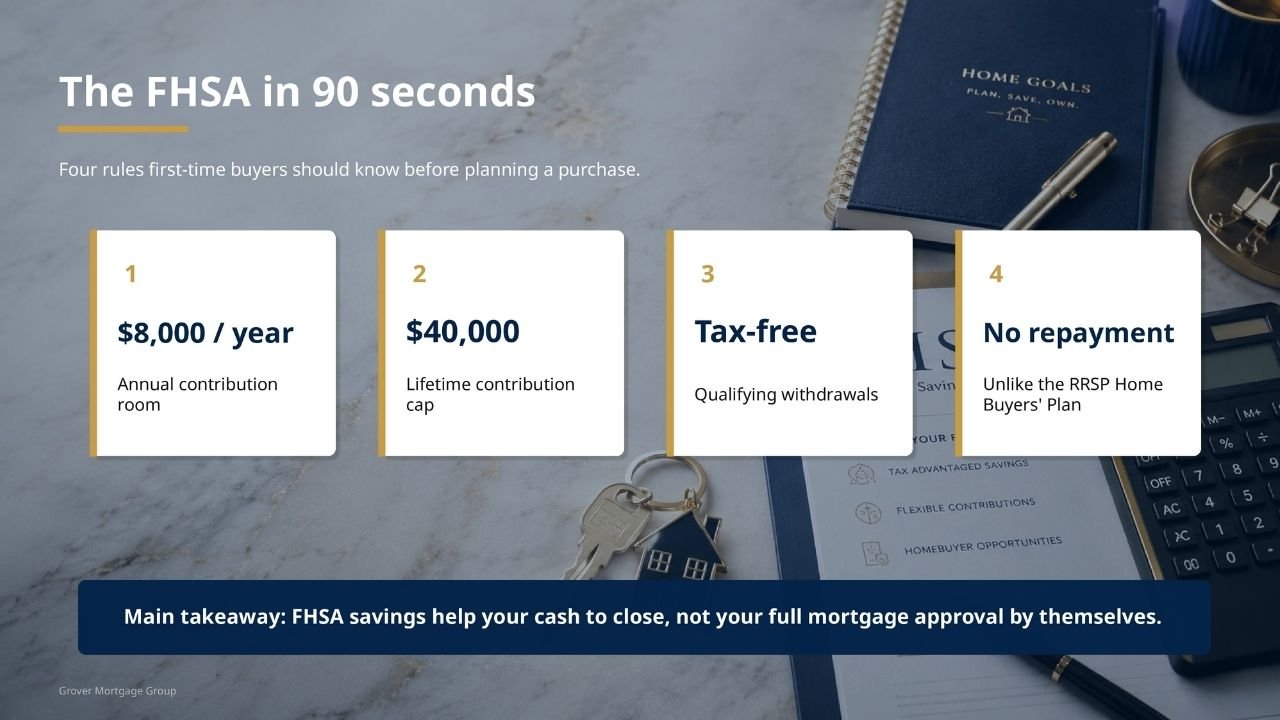

- Contribution room: Up to $8,000 per year, $40,000 lifetime.

- Tax benefit: Contributions may be tax-deductible, and qualifying withdrawals are tax-free.

- Big advantage: Unlike the RRSP Home Buyers’ Plan, FHSA withdrawals do not need to be repaid.

- The catch: It helps your down payment. It does not replace mortgage qualification.

Using your FHSA can help with your down payment, but it is only one part of preparing for your first mortgage. For full mortgage guidance before you buy, visit our main page for first-time home buyer mortgage broker in Mississauga.

Who Can Open an FHSA?

To open a first-time home savings account, the CRA requires you to meet a few conditions:

- You must be a Canadian resident.

- You must meet the age rules in your province.

- You must qualify as a first-time home buyer at the time you open the account.

- You must not have lived in a qualifying home that you or your spouse or common-law partner owned during the current year or the previous four calendar years.

That fourth point trips people up. If you currently live in a home that your spouse owns, you may not be considered a first time buyer for FHSA purposes, even if your name is not on title. The rule is about where you have lived, not just whose name is on the deed.

How Much Can You Contribute?

You can contribute up to $8,000 per year, with a lifetime cap of $40,000.

A few other things the CRA confirms:

- You can have more than one FHSA, but the contribution room is shared across all of them.

- The limit is per person, not per bank.

- Going over your limit creates penalties, so track your contributions carefully.

What the Tax Deduction Means for Your Down Payment

Contributions may be deducted from your taxable income, similar to an RRSP. That deduction often comes back to you as a tax refund.

For a first time buyer, that refund is not just extra money. It is fuel for your down payment plan. Reinvest it into your FHSA the following year. Set it aside for closing costs. Use it to clear a small debt before pre-approval.

From my side of the desk, the goal is simple: turn that refund into more buying power. For deeper tax timing questions, talk to a qualified accountant.

How FHSA Withdrawals Work When You Buy a Home

When you find your first home, you can withdraw your first time home savings account funds tax-free, as long as you meet the qualifying withdrawal rules:

- You must have a written agreement to buy or build a qualifying home in Canada.

- You must intend to occupy it as your principal residence within one year.

- You must be a Canadian resident at the time of the withdrawal.

A few things make the FHSA especially powerful at this stage. There is no minimum holding period. Even if you opened the account a few months ago, you may still be able to make a qualifying withdrawal. And unlike the RRSP Home Buyers’ Plan, you never have to repay the money.

That single rule, no repayment, is one of the biggest reasons I steer first-time buyers toward the FHSA first.

FHSA vs RRSP Home Buyers’ Plan

Both tools help you fund a first home. They work differently.

| Feature | FHSA | RRSP Home Buyers’ Plan |

| Tax-deductible contribution | Yes, within FHSA limits | Yes, under RRSP rules |

| Tax-free withdrawal for home | Yes, if qualifying | Yes, if HBP rules met |

| Repayment required | No | Yes |

| Current limit | $40,000 lifetime | $60,000 withdrawal |

The good news: you do not have to pick just one. The CRA confirms you can use both for the same qualifying home, provided you meet the conditions for each. For couples, both partners can have their own FHSA and their own HBP withdrawal. Layered correctly, that can mean a much stronger down payment.

How the FHSA Fits Into Mortgage Approval

This is where most FHSA articles stop being useful.

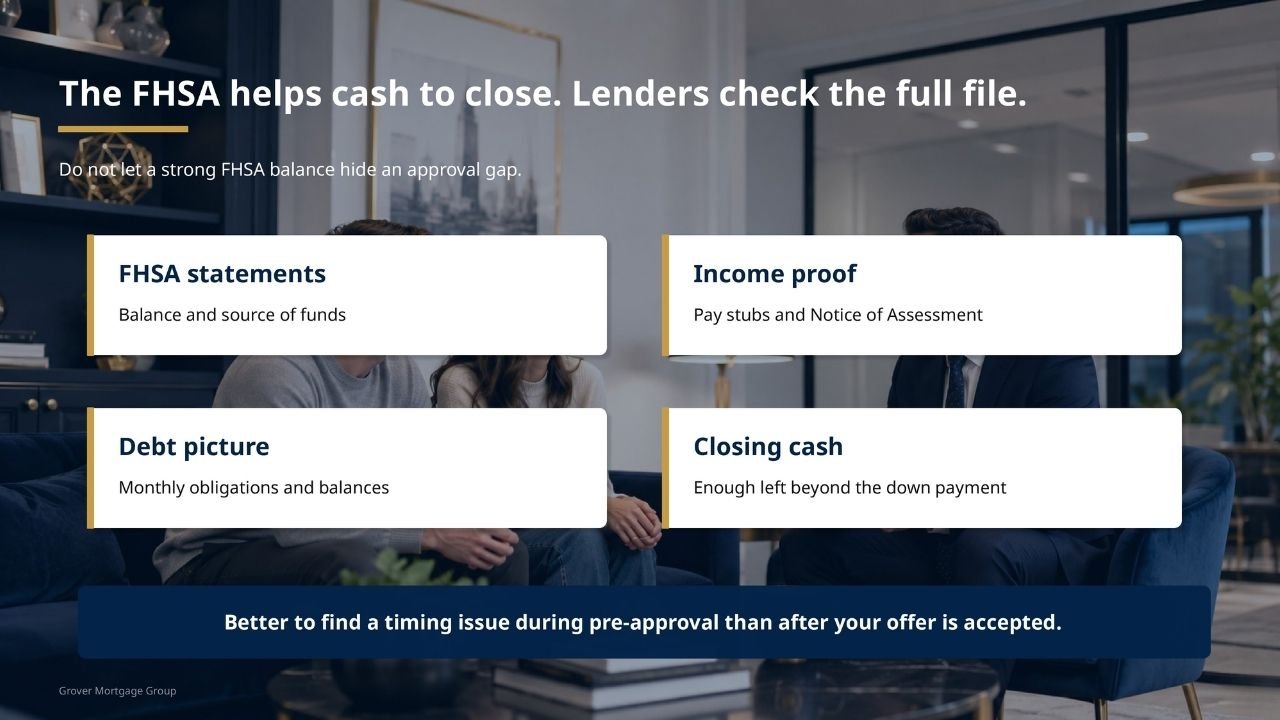

Lenders care about more than how much you saved. They want to know where the down payment came from, how long it has been there, and whether anything else in your file affects approval. When you use FHSA funds, I will ask you to provide:

- Recent FHSA statements showing the balance and source of funds

- Proof of income, usually pay stubs and a Notice of Assessment

- A clear picture of your existing debts and monthly obligations

- Confirmation that you have enough left for closing costs

Your FHSA helps your cash to close. It does not fix a weak file. In my pre-approval guide for first-time buyers, I walk through how lenders review the full picture.

Honestly, I would rather see your FHSA statement during pre-approval than discover a timing issue after the offer is accepted.

Common FHSA Mistakes I See

Opening the account too late

The contribution room only starts when the account is open. Waiting until you are house shopping costs you years of potential room. Open it now, even if you only contribute a small amount.

Overcontributing

The annual and lifetime limits are firm. If you have multiple FHSAs or maxed out earlier in the year, double check before adding more.

Forgetting closing costs

Down payment is not the only cash you need. Legal fees, land transfer tax, title insurance, home inspection, and adjustments add up fast.

Withdrawing at the wrong moment

The FHSA only stays tax-free when your withdrawal lines up with the qualifying rules, which means timing it around your signed purchase agreement and your closing date. I help clients sequence this during the offer.

Thinking FHSA approval means mortgage approval

Your bank can approve your FHSA in ten minutes. Your mortgage lender will still review your full file. Two separate processes, and I have watched buyers confuse them at the worst possible moment.

When Should You Open an FHSA?

You should open a first-time home savings account as soon as you are eligible and seriously thinking about buying a home, even if that purchase is years away. Opening early gives you more room, more flexibility, and more time for tax-free growth. You do not need to max out the $8,000 right away. Just start the clock.

One caution: money you may need within a year or two should not be invested aggressively. A down payment is not retirement money. Pick investments that match your timeline.

What Happens If You Do Not Buy a Home?

The CRA sets a maximum participation period, which ends on the earliest of the 15th anniversary of opening your first FHSA, the year you turn 71, or the year after your first qualifying withdrawal.

If you do not buy a home, your FHSA savings can usually be moved into your RRSP without losing the tax advantages, as long as it is handled properly. Your savings are not stranded. They just shift into a different vehicle. Your accountant can walk you through the mechanics if it comes to that.

The FHSA Is One Piece of the Puzzle

Every dollar toward your down payment matters, and the FHSA gives you a real edge. But your down payment is only one piece of what gets you to the closing table.

If you are buying a condo, your lender will factor in monthly maintenance fees. For a freehold home, property taxes and heating costs come into play. Mortgage insurance applies on most files with less than 20 percent down. Your existing debts, even small ones, can move your approval limit.

A bigger down payment helps. The full approval picture is what gets the keys in your hand.

Let Us Build the Plan Together

Before you start guessing what you can afford, let us look at the full picture. Your FHSA is one part of the plan. The mortgage approval is the part that makes the plan real.

I work with first-time buyers across Mississauga, Oakville, Burlington and the GTA.

Book a free first-time buyer consultation with me before you start shopping. Send me your income details, estimated savings, FHSA balance, and timeline, and I will take it from there.

The first home is the hardest one. Let us make sure yours is the one you will look back on with a smile.